Related Articles

The moment I first held the Scapia credit card, I knew this was not just another plastic in my wallet. Over recent years of frequent international travel, I have tested many travel cards and wallets, but the Scapia credit card intrigued me because it promised zero forex fees and a dual card setup. As someone who journeys across continents (I guess it’s fair to say that since I’ve been on the move since 2023) for work, I was eager to find a card that could seamlessly bridge my domestic and international spending needs without burning a hole in my pocket.

Let me start with what I call my “Sri Lanka ATM moment.” I was invited to speak at KCD Sri Lanka, my first international KCD event. For the trip, I took about LKR 15,000 in cash, thinking that would be enough for the initial days. Rookie mistake. Sri Lanka loves cash. By day one, I was left with barely any cash and suddenly found myself on a mini-hunt for an ATM.

That’s when I truly experienced the potential of my Scapia credit card. I found a Visa ATM and withdrew LKR 22,000. The transaction fee was Rs 500 plus 18% GST, which felt a bit steep initially. But here’s the catch: I repaid the amount instantly, and because it was a credit card withdrawal, I didn’t pay any interest. The math worked out better than I expected compared to typical forex or cash advance fees on other cards.

Why This Review Stands Apart

But first things first, why does this review of the Scapia Credit Card stand apart?

Countless Scapia credit card reviews are floating around the internet. Most just list features, benefits, and fee structures. But I wanted this review to be different. This is not about marketing jargon or flashy promises. Instead, I’m sharing my real travel experiences with the card across multiple cities and continents.

Whether it was tapping my card in the bustling markets of Lima or withdrawing cash from a Visa ATM in Colombo, I’ll walk you through exactly how the Scapia card performed. This is about practical use, hiccups, and the little wins that make or break your travel payment experience.

So buckle up for a detailed, honest, and no-fluff account of how one card tried to keep up with me across six very different countries.

What is Scapia, and Why I Got It?

Before diving into travel stories, let me give you some background on the card itself and why I chose it.

I used Niyo Global before this, a card I got on my first US trip in 2023. It worked perfectly fine initially. But then their relationship with Equitas Bank went south, and since I had a debit card with them, closing the account and card became a hassle. It took weeks of back and forth, which honestly got tiring. So, I started looking for a credit card option with zero forex fees that could work internationally without drama.

Enter Scapia. It’s a co-branded credit card with Federal Bank, and the biggest selling point for me was the promise of zero forex markup. Plus, it is lifetime free: no annual fee, which means no pressure to hit a certain spend threshold just to justify owning it.

Another interesting feature is the dual card setup. When you get Scapia, you receive both a Visa and a RuPay card – each with its own benefits. The Visa card is great for international use, while the RuPay card has unique advantages domestically, especially when linked with UPI payments.

With zero forex fees and a dual card setup, Scapia seemed like a perfect fit for both my frequent international travels and everyday India spending.

Plus, the application process was fairly simple. Downloaded their app, created an account, did the video KYC, and it was approved the same day. The card was activated almost instantly after approval, but the physical card was delivered in like 3 days. And loved the packaging!

Real World Use: Country by Country

It’s been just a year or so since I’ve been using the Scapia Credit Card, and fortunately, 2025 was a year of international travel for me. Started with Dubai with parents in February, London for KubeCon in early April, extended that with Scotland and Turkey, Las Vegas in September, Sri Lanka in October, Kubecon Atlanta in November and Peru in December – yes, a lot of blog posts are pending, I’m way behind schedule here, but you can check my Instagram profile for highlights of each trip.

Mexico

Most recently, I had the opportunity to visit Mexico. I was there for a work retreat in the city of Cancun, but I also spent a few days in Mexico City. The Scapia credit card worked out pretty well without any issues. The Mexico City metro has tap-and-pay available, so you can tap your Scapia credit card and get on the metro. The fixed fare is MXN $20 for every trip. Apart from that, the credit card worked well at places like 7-Eleven, OXXO and other convenience stores.

One thing to note is that a lot of small markets Mercados accept mostly cash, so ensure to take some cash with you. I was short of cash, so I tried taking cash from the ATM using the Scapia credit card, but most places were charging a convenience fee ranging from MXN $30 to MXN $90 for a withdrawal of MXN $1000, which I felt was steep! The good part was that I wasn’t charged anything by Scapia for just inserting the card in the ATM machine and not withdrawing cash.

Japan

I was in Japan a few weeks ago, and Scapia was the only card I used left-right-centre. It was accepted everywhere I visited, from the Asics and Uniqlo flagship stores to my hostels and 7-Eleven, Lawsons, etc. The tap-and-pay functionality was glitch-free, and the card worked all the time.

Yes, I had limits applied from the app on the amount of the transaction, so it was declined a couple of times, but that’s another good part of the app and the controls. As I mentioned in the first time Japan itinerary blog post, Japan, like Sri Lanka, needs cash. I had a sufficient amount with me, and didn’t have to visit an ATM for cash.

Sri Lanka

As I mentioned earlier, the ATM withdrawal was my first real experience with Scapia abroad. I withdrew LKR 22,000 from a Visa ATM. The fee charged was Rs 500 plus 18% GST, which initially felt steep, but remember this was an instant repayment on a credit card. So there was no interest, which made the cost manageable compared to standard forex or cash advance fees on other cards.

I also used the tap-and-pay feature at hotels and restaurants. Sri Lanka has a mixed payment culture: cash is king, but bigger hotels and restaurants happily accept cards. This worked well with Scapia; no declined transactions or hidden charges.

Turkey

Turkey was a delight from a card usage perspective. Contactless and tap-to-pay worked flawlessly in Istanbul and Cappadocia. In fact, I barely had to use cash except for a few small local shops and street vendors.

Here’s what I noticed: Scapia’s Visa card was accepted almost everywhere. From cafes to museums and even public transport, tap and pay worked about 99% of the time. I loved how convenient it was not to worry about carrying Turkish lira notes constantly.

Still, a small note: Some local markets and smaller vendors preferred cash, so it’s always good to carry some lira just in case.

Peru

Peru was a reality check on cash-heavy countries. In Lima and Cusco, local markets still function predominantly on cash. Some places had PayTM-like machines showing QR codes for payments, but they charged an extra 2-5% fee for card payments, which was annoying.

Restaurants, however, accepted cards just fine. I used the Scapia credit card comfortably in Lima, Cusco, and even Machu Picchu, where I booked tours and meals. (By the way, my detailed Peru blog posts are still in the works, but you can check out my Instagram highlights here: Instagram Highlights)

Visa acceptance in Lima was decent but not as widespread as in bigger cities worldwide. So, having some cash was necessary, but Scapia covered all my restaurant bills and hotel stays without a hiccup.

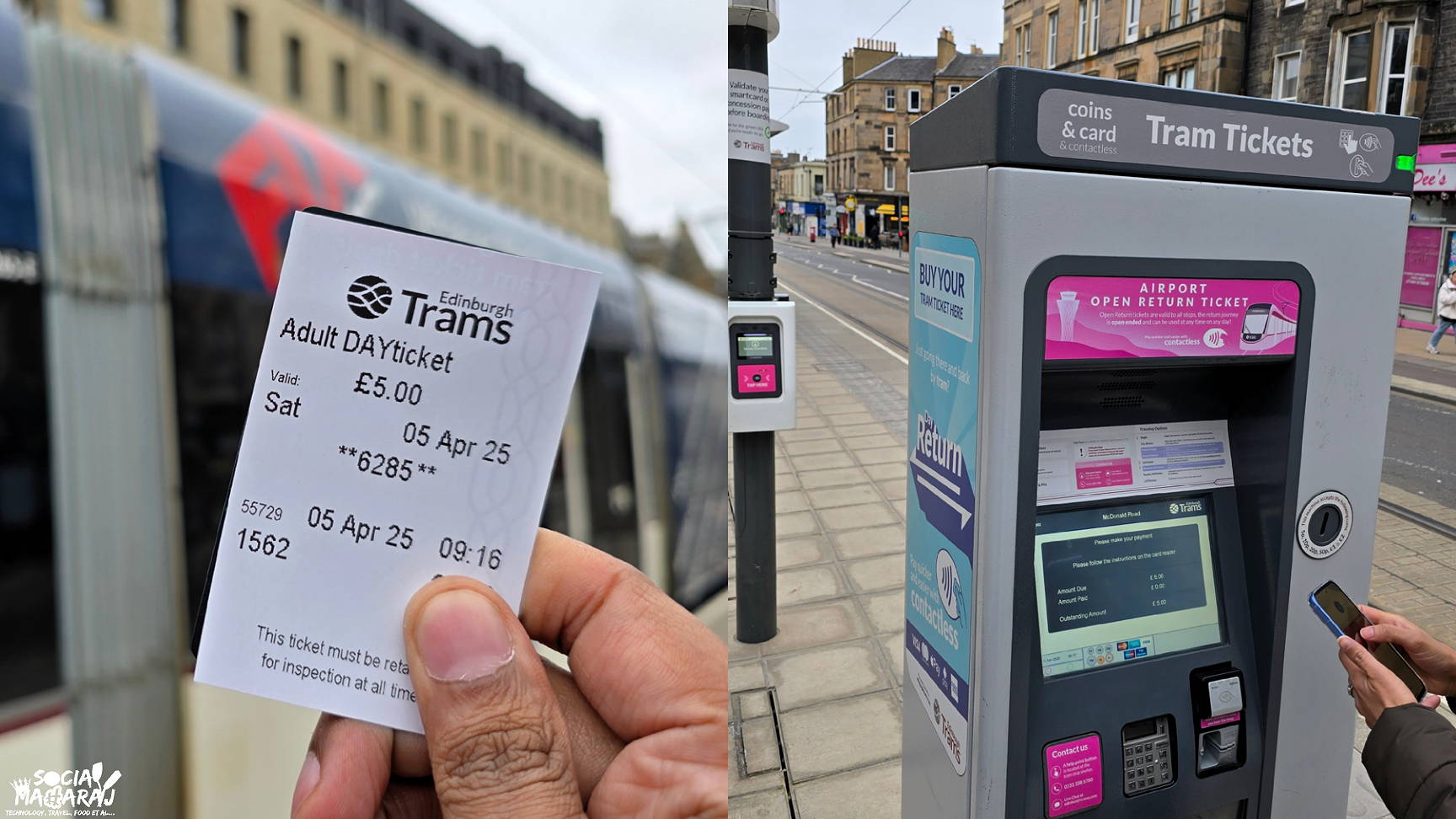

Scotland and United Kingdom

Card use was smooth sailing in the UK and Scotland. I used contactless payments on public transport such as trams and the Liner train, including buying onboard beverages. Everything worked perfectly.

If you want to read about my Scotland adventures, check out the Scotland Tag on my blog and for London, here’s the London Tag.

London and Europe, in general, are very card-heavy places. Many spots like the Borough Market only accept card payments, so having a reliable international card is critical. Scapia worked with zero issues for everyday spending, from coffee shops to groceries, with no friction or delays at the checkout.

United States

In the US, I used the card in Atlanta Metro, Salt Lake City, and Las Vegas. Generally, card usage was straightforward and smooth. Tap and pay worked as expected.

However, I ran into a frustrating problem with Samsung Wallet on my Galaxy S24 Ultra – it refused to add the Scapia credit card. I suspect it’s because the phone’s OS is set to a US locale. Even UPI apps don’t work on it for me, so this was a bummer.

Unfortunately, I couldn’t find a workaround either. So if you’re planning to use the Scapia card with Samsung Wallet on US-bought Android phones, be warned that it might not work smoothly yet.

Domestic Use: The Lounge Story

One of the perks of Scapia credit card is free lounge access. I managed 6 lounge visits in a single month across Delhi, Hyderabad, and Bangalore airports.

Here’s how it works: To unlock lounge access, you need to spend Rs 20,000 in a billing cycle, as per the new 2026 update. Earlier, the threshold was Rs 15,000 for the RuPay variant and Rs 10,000 for Visa, but now it’s combined for both cards, which is simpler.

A caveat: Lounge access is limited to domestic terminals only. For example, at Hyderabad’s Aero Plaza, many restaurants are listed as part of the program, but I couldn’t dine there because I had an international boarding pass. You also need to enable location and upload your boarding pass in the app for access.

The QR code process via the app at the lounge gate is super smooth. Instead of fumbling to figure out which card works or showing boarding passes physically, you just scan the QR code, and you’re in. It really speeds up the process and feels modern.

The RuPay Add-On Card

The RuPay card is an underrated gem in the Scapia package. I opted only for a virtual RuPay card and linked it with Cred UPI. This means that all places accepting credit card-linked UPI payments automatically default to my RuPay card.

This is a big deal because it earns me Scapia coins on everyday spending in India and works at most places without any hassle.

Many people underestimate RuPay credit cards for daily spending, but in my experience, this card setup is powerful for Indians who want to maximise rewards and convenience without juggling multiple cards.

The Honest Cons

Now, I won’t lie, Scapia credit card is not perfect. Here are the honest downsides I encountered:

- Approval Process Is Unpredictable: I referred many friends and colleagues, but a good number of them got rejected. So the approval criteria are a bit mysterious and inconsistent.

- Samsung Wallet Incompatibility: Especially on US-bought Android phones like my Galaxy S24 Ultra, the card doesn’t add to Samsung Wallet. Even UPI apps struggle on such devices, which limits tap-and-pay options via smartphones abroad.

- Points Locked to Scapia App Only: The reward points or coins earned with this card cannot be transferred to other loyalty programs like Marriott Bonvoy. I wish they had more flexibility like American Express rewards, where you can transfer points to hotel programs.

- No Rewards on International Spend: Surprisingly, the card does not earn rewards on international transactions. This is a bit of a bummer for a travel card, but understandable given the zero forex fee feature.

The Points System: My Take

Let me break down how the points system works with Scapia.

- You earn 10% coins on domestic spending.

- If you book through the Scapia app, you get 20% coins.

I have not redeemed my coins yet because I haven’t found anything compelling enough to spend them on. The coins are valid for 3 years, so I’m still watching how this plays out over time.

The points system feels decent for domestic spending, but the lack of international rewards is a missed opportunity for frequent travellers.

Final Verdict

So, who is the Scapia credit card for?

- If you are a frequent traveller who spends both domestically and internationally, this card is worth considering. The zero forex fee, lifetime free status, and dual card setup make it a very practical choice.

- If you want a card that works well across multiple countries and currencies without annoying forex markup, this is a strong contender.

- The lounge access benefit is a nice bonus for domestic travellers.

- The RuPay card’s UPI integration is underrated and valuable for everyday Indian spending.

Who should look elsewhere?

- If you want a robust rewards program with flexible point transfers, this might not be your best bet.

- If you rely heavily on Samsung Wallet for tap and pay abroad, especially with US-bought Android phones, you may face issues.

- If you want rewards on international spends, look at other premium travel credit cards.

Finally, the zero annual fee means the risk is low. You can try it out without worrying about paying a fee upfront.

How to Apply

If you’re convinced and want to try Scapia credit card, you can apply via my referral link. You get 1000 coins on approval, which is a nice little head start.

If you have any queries or suggestions, drop them in the comments below. You can also tweet to me at @Atulmaharaj or DM @Atulmaharaj on Instagram or Get In Touch.

Lost Scapia Card

I never thought I’d be writing this, but I lost my Scapia Credit Card at Cancun Airport. I was on a video call at home, was also eyeing the luggage on the luggage belt, rushing to the washroom and booking a cab, amidst all of this, I dropped the card from my pyjama’s pocket. While I went back inside the terminal to find it, I couldn’t.

The first step now was to block the credit card. The Scapia mobile app worked well here. I simply locked the card instead of blocking it. I wasn’t sure if the Rupay would be blocked, too. Once I was at home in India, I blocked the card and got a Scapia replacement card. The company charged Rs 200 + GST (18%) for the replacement credit card. The blocking was instant and the card was delivered in 3 days. And setting up the replacement card was also pretty easy.

Quick Facts At a Glance

- Card Type: Co-branded Federal Bank Scapia Credit Card (Visa + RuPay)

- Annual Fee: Lifetime free

- Forex Markup: Zero forex fees on international spends

- Lounge Access: Domestic airport lounges, Rs 20,000 monthly spend threshold (2026 update)

- Rewards: 10% coins on domestic spends, 20% coins on Scapia app bookings, no international rewards

- Unique Features: Dual card setup, UPI payments via RuPay credit card

- Known Issues: Samsung Wallet incompatibility on US-bought Android phones, unpredictable approval process